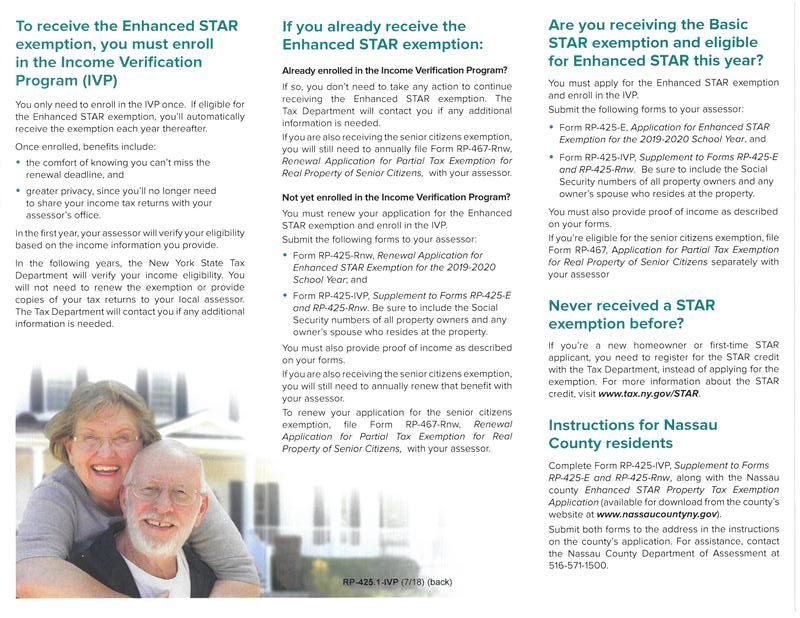

Tax collector

Tax Collector:

Kathleen Robertson

53 Osawentha Drive, Lewis, NY 12950

Home Phone : (518) 873-9818

Kathleen Robertson

53 Osawentha Drive, Lewis, NY 12950

Home Phone : (518) 873-9818

The Tentative Assessment Roll is on file and may be viewed at the Lewis Town Hall, Monday thru Friday from 7:30 am - 3:30 pm beginning May 1, 2024.

The assessor will be in attendance with the Tentative Roll at the Lewis Town Hall on the following dates and times:

May 4 6pm - 10 pm

May 10 Noon - 4 pm

May 17 Noon - 4 pm

May 24 Noon - 4 pm

Grievance Day is May 28th, 2024 from 4 pm - 8 pm at the Lewis Town Hall.

The assessor will be in attendance with the Tentative Roll at the Lewis Town Hall on the following dates and times:

May 4 6pm - 10 pm

May 10 Noon - 4 pm

May 17 Noon - 4 pm

May 24 Noon - 4 pm

Grievance Day is May 28th, 2024 from 4 pm - 8 pm at the Lewis Town Hall.

Municipal-wide reassessments are the best way to ensure that assessments are fair and accurate

During a reassessment, the assessor (or a hired contractor) will review the market values of all of the properties in the community. Based on changes in the real estate market, the assessor will determine which assessments need to be increased or decreased.

According to Real Property Tax Law (RPTL) 102 (12a), Revaluation, reassessment or update means a "systematic review of the assessments of all locally assessed properties…

What does this mean in simpler terms? RPTL 305 requires that all assessments be at a uniform percentage of value - i.e., the same "level of assessment" (LOA). The only way to ensure that all properties are assessed at the same LOA is to analyze each assessment with respect to the current market at a specific point in time (the valuation date), and then to adjust the assessments as necessary to achieve equity and/or a desired LOA. It does not necessarily mean that all assessments will increase, or even be changed.

Why do equalization rates need to be established each year? The Real Property Tax Law requires that annual State equalization rates be established for each county, city, town, and village. Equalization rates are calculated each year to reflect that year’s assessment roll and current market values for each assessing unit.

What are equalization rates used for? Aside from apportionment of taxes among municipal segments of school districts and counties, and distribution of state aid for education, some of the less recognized uses of equalization rates include:

● establishment of tax and debt limits;

● allocation of costs, such as for jointly-operated hospitals among participating localities or an injury to a volunteer firefighter, among others;

● determination of state assessments (special franchise) or approval of local assessments (state-owned land);

● determination of ceilings (railroad and agricultural values) and exemptions;

● determination of level of STAR exemptions;

● apportionment of sales tax revenues and joint indebtedness; and

● as evidence in court proceedings on the issue of assessment inequity and small claims assessment review hearings.

During a reassessment, the assessor (or a hired contractor) will review the market values of all of the properties in the community. Based on changes in the real estate market, the assessor will determine which assessments need to be increased or decreased.

According to Real Property Tax Law (RPTL) 102 (12a), Revaluation, reassessment or update means a "systematic review of the assessments of all locally assessed properties…

What does this mean in simpler terms? RPTL 305 requires that all assessments be at a uniform percentage of value - i.e., the same "level of assessment" (LOA). The only way to ensure that all properties are assessed at the same LOA is to analyze each assessment with respect to the current market at a specific point in time (the valuation date), and then to adjust the assessments as necessary to achieve equity and/or a desired LOA. It does not necessarily mean that all assessments will increase, or even be changed.

Why do equalization rates need to be established each year? The Real Property Tax Law requires that annual State equalization rates be established for each county, city, town, and village. Equalization rates are calculated each year to reflect that year’s assessment roll and current market values for each assessing unit.

What are equalization rates used for? Aside from apportionment of taxes among municipal segments of school districts and counties, and distribution of state aid for education, some of the less recognized uses of equalization rates include:

● establishment of tax and debt limits;

● allocation of costs, such as for jointly-operated hospitals among participating localities or an injury to a volunteer firefighter, among others;

● determination of state assessments (special franchise) or approval of local assessments (state-owned land);

● determination of ceilings (railroad and agricultural values) and exemptions;

● determination of level of STAR exemptions;

● apportionment of sales tax revenues and joint indebtedness; and

● as evidence in court proceedings on the issue of assessment inequity and small claims assessment review hearings.